")

What is the VAT reverse charge for building and construction services?

The VAT reverse charge shifts the obligation to account to HMRC for output tax on a supply from the supplier to the customer.

From 1 March 2021 the charge must be applied to standard and reduced-rate VAT services:

- for individuals or businesses who are registered for VAT in the UK

- reported within the Construction Industry Scheme (CIS)

These new rules are being introduced as an anti-fraud measure to prevent a supplier being paid VAT for goods and services supplied and then ‘running off’ with it before it’s declared to HMRC.

Action you can take to be ready by 1 March 2021

- Check what construction services you must use the reverse charge for

- Watch our recorded webinar by VAT expert, Neil Owen

- Read our more detailed guidance on the construction sector VAT reverse charge

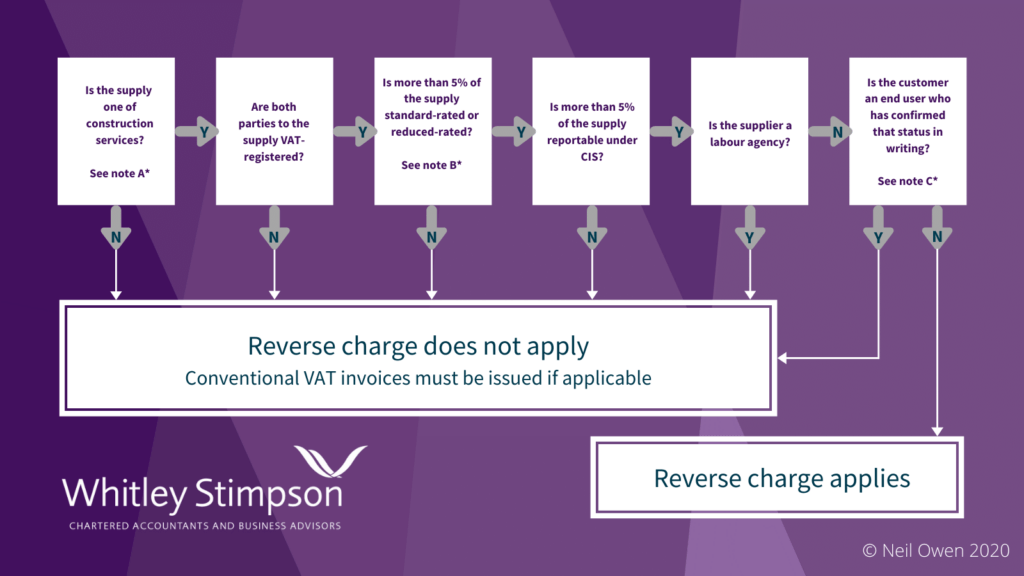

- Use our helpful flowchart to help you decide if you need to use the reverse charge

*Note A, B, and C can be found at the end of page 4 of the Note on the construction sector VAT reverse charge

More information on VAT reverse charge

Further information can be found on the GOV.UK website using the following links:

- VAT reverse charge technical guide

- How to use the VAT reverse charge if you supply building and construction services

- Check when you must use the VAT reverse charge for building and construction services