From the 2024-25 tax year, self-employed individuals with profits in excess of £6,725 no longer need to pay Class 2 NICs. Instead those taxpayers will receive a National Insurance credit to secure their access to contributory benefits such as the state pension....

If you reimburse fuel or charging costs for employees using a company car for business travel there will be no taxable profit and no Class 1A National Insurance, provided the mileage amount paid does not exceed the advisory rates. From 1 September 2025 the advisory...

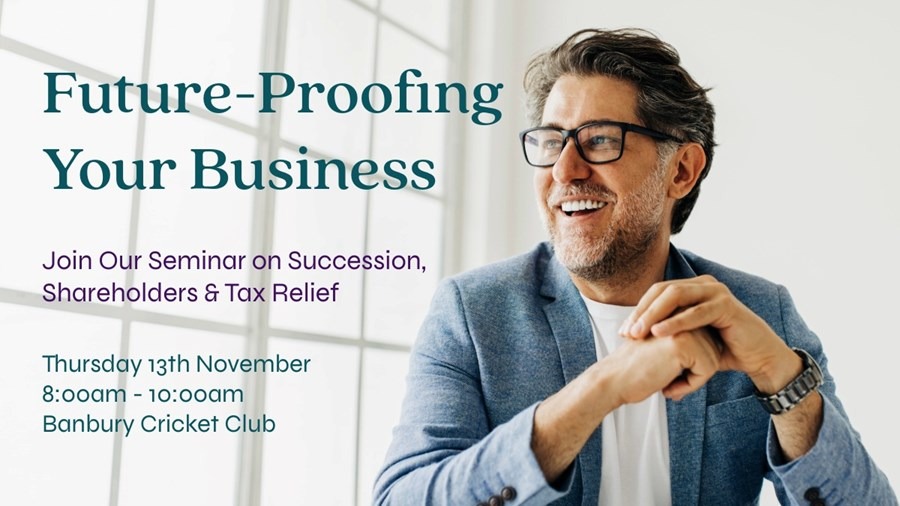

Prepare your business for its next chapter with practical insights from Whitley Stimpson and SE-Solicitors. This future proofing your business seminar will explore how to effectively manage succession planning, introduce new shareholders, and make the most of...

Making Tax Digital for Income Tax (MTD IT) is fast approaching, with the mandation date for sole traders and landlords with qualifying income of £50,000 and above set firmly at 6 April 2026. In addition to the annual tax return, those mandated to comply with the MTD...

Accountants and business advisors, Whitley Stimpson, reports a significant shift in the property investment landscape as more landlords opt to register as limited companies. This trend is driven by recent tax changes and rising interest rates, which have made...

With changes to employer’s National Insurance and the Employment Allowance, now is the time for businesses to review the most tax efficient mix of salary and dividends for directors. From 6 April 2025 the secondary Class 1 National Insurance threshold reduces from...